Updated version of this post is here. Buying health insurance – Comparison of 5 plans

I thought investing in mutual funds was a huge problem for you and me. Turns out I was so wrong.

Buying Health Insurance is a much bigger pain. I guess climbing the Everest would be easier. I don’t know from which planet did the creators of health insurance products come, but they have succeeded in scaring the hell out of us.

When the plans are presented to common janta like you and me, all I can feel is heads spinning.

Room rent capping, disease wise sub limits, waiting period for specific diseases and pre-existing diseases, co-payments, domiciliary hospitalisation, organ donor, emergency ambulance, renewals, no-claim bonus, refills, super top ups, top ups, vaccination, ….(stop for breathing…), how many things one needs to look at before deciding what makes sense?

I have spent over 24 hours (real hours) reading, talking and absorbing details on various health insurance websites and the plans they have to offer. Frankly, I am yet to recover.

Now I agree that there is a ton of useful material out there that already details what you should look for in buying health insurance. Even after going through those super helpful guides the evaluation of health insurance plans is simply no fun.

Anyways, after much dilly dallying, I decided to take the bull by the horns.

What was I looking for when buying health insurance?

I already hold a family floater policy (covers 2 of us) with a sum insured of Rs. 5 lacs from a PSU. The policy has been in force since 2007. But it has several limitations with respect to what you can do with it and how you can use it.

I am now looking for a health insurance policy that would give me similar cover without binding me with unnecessary terms and conditions of sub-limits, room rent capping, co-payment, etc.

I understand I may not be able to escape all the jargon and the Terms & Conditions, but the fewer they can be, the better it is.

I had to look at various companies and their offerings. I also contacted a few of them. The people I spoke to, I must admit, were very good. I was more informed after my conversations.

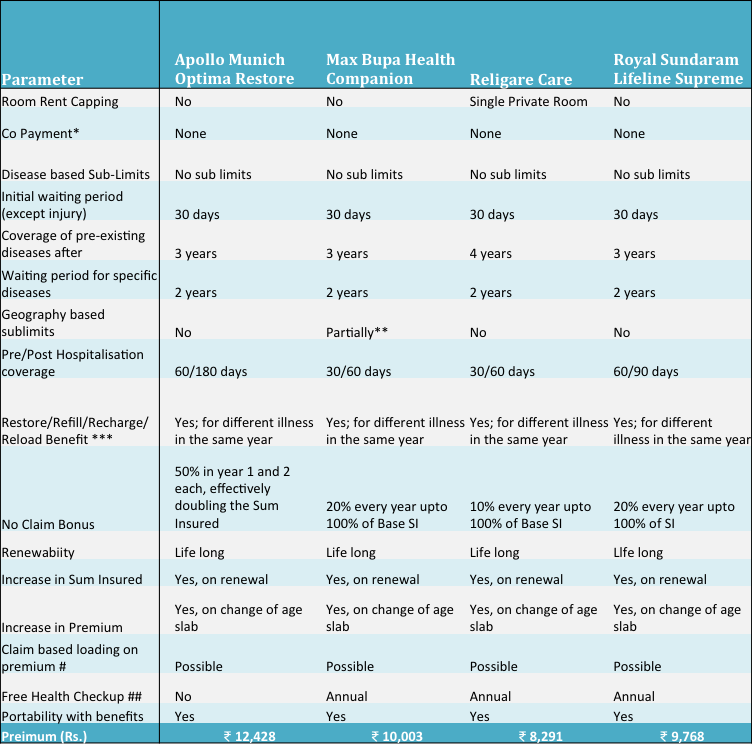

I used all the chats and the literature I read to prepare a comparison of 4 of those plans. In the table below, you can see their comparison against some critical parameters.

Buying Health Insurance – Comparison of 4 plans

The parameters are applicable for Rs. 5 lac floater policy for 2 people of age – 36 and 35 years.

Royal Sundaram Lifeline Supreme added to the comparison on July 4, 2016.

*In Religare, if you take a policy after 61 years of age, 20% co-payment is applicable.

**In Max, 20% co-payment has to be made by Zone 2 customers (basically those living in non metro cities). You get a 10% discount on premium for this.

***Restore is for Apollo, Refill is for Max, Auto Recharge is for Religare, Reload is for Royal Sundaram – functionally all are almost the same. Except for Apollo, the Restore option gets triggered only after the Sum Insured and the Bonus is exhausted.

#The insurance companies say that there is claim based loading of premium, that is, the fact that you have made a claim or developed a disease, the company would not increase premium for that reason. But the policy terms and conditions clearly specify that they could do risk based loading and the user has the choice to continue or not.

##In case of Apollo, free health checkup is only available for policies with Sum Insured greater than Rs. 15 lacs.

In case of Royal Sundaram, 15% discount on premium is available for customers in Zone 2 (as defined by the company).

Note: The premium would change for change in sum insured, no. of people covered, age of the insured, other benefits sought, etc.

OK. Here are some pointers to make sense of the table:

- All the policies have practically no capping or sub limits on room rents or specific diseases. This removes the biggest hassle. I need not look at the hospital’s menu card every time and decide what I want to have or not. When it comes to medical attention, I want no compromises. None at all.

- There is no co-payment required to be done ever. My claim would be fully reimbursed. Only in Max’s case, it you are not from a zone that they have specified, there could be a 20% co-payment.

- One of the most important features of all the 3 policies is the Restore/Refill/Recharge. What it means is that if I exhaust my Sum Insured in any year in a claim, the insurance company will restore/refill/recharge the policy for the full Sum Insured again. But it cannot be claimed for the same illness by the same person again in the same year. It can only be used for a new illness or by the other insured person.

- The No Claim Bonus is earned at the end of a year if you have not made any claims on the policy. It is very attractive in the case of Apollo. In case of Religare, they have an option of Super No Claim Bonus which can take your cover higher by 150% over 5 years. This comes at a slightly higher premium. Royal Sundaram in its Lifeline Supreme option offers 20% NCB every year (till 100% of Sum Insured).

- Renewability is assured life-long by law. So, that is not the concern.

- You can port your existing policy to any of these insurance plans and also carry forward any benefits that you have accrued so far.

- The biggest difference is in the premium, with Apollo coming across as the most expensive and Religare the cheapest. However, if you are from Zone 2 as defined by Royal Sundaram you get a 15% discount on the premium which could make it close to Religare’s. And this is when there is no significant difference in the features being offered. Typically, premiums are lower or higher based on the features offered, caps or limits applicable, but that is not the case here.

- As you can see I have not included coverage of network hospitals in the comparison. Most policies have a wide network of hospitals. In this case all the 3 claimed to have over 4000 hospitals, pan India, in their network. However, it would be great if you could find out which hospitals closer to your area are part of the company’s network. They are what you will likely use the most.

- There are other parameters like organ donation, emergency ambulance, vaccination against animal bites, etc. but again I would not consider them critical inputs to make a selection for buying health insurance.

Read more: What is a top up health insurance?

I call upon you too to share your feedback and inputs.

If you have had an experience with the insurance claim process, please be kind to share that as well.

By the way, which one would you choose out of the 4 listed above?

Here are web links on the 4 health insurance plans compared above. Click for more information.

- Apollo Munich Optima Restore

- Max Bupa Health Companion

- Religare Care

- Royal Sundaram Lifeline Supreme

Disclaimer: The above comparison has been carried out only for study and analysis purposes. This should not be taken as a recommendation. You should consult your advisor and communicate your specific needs and then select a policy best suited to it. The author is not registered with IRDA or any insurance company.

Read further: Buying Term Plan – Comparison & Key Questions

Hi Vipin,

Which is the best Super Top Up Policy available in the market? Can you please do a detailed comparision of Super Top Up Policies? Also which is the best available health insurance in the market for age 60? Currently I am covered with Apollo Munich Standard Policy for 3 lakhs which I want to increase to 5-7 lakhs?

Hi Yogesh, have you considered the Apollo Optima Super Top up?

Hi,

I am of 49 years age and my wife 46. Is it advisable to go for family floater or individual health policies for both?

Unless you fall into two different slabs resulting in a higher premium, you can go for a floater policy.

Hello Vipin,

Is there any health policy I can purchase after having undergone treatment for cancer (surgery followed by chemotherapy). As of now there is full recovery and no evidence of disease.

Thanks,

N Shah

Unfortunately, NO. There is none. However, if you are covered under Group Insurance of your organisation, there is a chance that you can get coverage. You should check.

Hi Vipin

I am newly married and I want to buy a health insurance for me (30 yrs) and my wife(29 years) . After a week of extensive research we have zeroed on MAX Bupa Health companion and Apollo Munich Optima Restore.

1. Can u please suggest which one is better? and also the reason for the same.

2. What is the optimum cover for the medical insurance?

Thanks

Raj

Hello Raj

Based on the inputs in the article, I am sure you understand what is on offer in the policies you have shortlisted.

What features or advantages matter to you?

As for the coverage, you should have at least 5 lacs of coverage. With the refill coverage, you get another 5 lakhs for a different disease.

Keep evaluating your cover every few years and increase it in line with the change in medical treatment costs.

Hope this clarifies.

hi Vipin

Thanks for the prompt reply. My Problem is that I am unable to find any difference between Max Bupa and Apollo plan and both have the similar features and benefits which I require. What I am not able to understand is why Apollo ‘s premium when compared to Max is almost 2500 higher for my Age bracket. Is there a catch in the Max policy? or is Apollo a better company than Max when it comes to claim settlement and customer service that why its charging a higher premium.

Raj,

If you see the comparison table carefully, Apollo scores over Max on several parameters, including yearly increase in Sum Assured, Pre/post hospitalisation coverage, geography based sub limits. However, Apollo does not offer free yearly health checkups below Rs. 15 lacs of cover.

Thanks for the reply.

I agree with the comparison table.However, on sum assured criteria, there is a catch in Apollo. Incase of claim the bonus per year reduces to 50% of the original value whereas it doesn’t impact incase of Max.

Anyways, I will read the policy wordings of each and will go ahead with the one most suitable for my family.

One important tip I have for you Vipin is that one of the most imp thing which you haven’t considered are the ICR (Incurred Claim Ratio) and CSR(Claim Settlement Ratio) for all the companies. IRDA publishes this info and this can also be found on the balance sheet of these comapnies. Would request you to add that also since without those important parameters this table is not sufficient for customers to make an informed decision.

Thanks

Raj

Thanks for the feedback Raj. In a competitive market, no company can afford to mess up its genuine claims ratio.

Hi,

Though a new user, I believed that my query was a follow-on to Raj’s latest comment on this thread (with my interest on Royal Sundaram General-Lifeline Supreme). Hence, my decision to post it here.

Vipin, it is my general belief that LIFELINE is a good policy. My concern was regarding to two stats of the policy mentioned below.

a. CLAIMS PENDING FOR OVER 6 MONTHS (% OF CLAIMS PENDING AS OF 31 DEC 2014) which is 21%

http://www.livemint.com/templates/health/Family%20Floater%20Plan20lac-35yrs

b. Incurred Claim Ratio of the Insurer being 52.89%

https://www.bankbazaar.com/health-insurance/top-health-insurance-plans-india.html

1. Can you please comment on the above and how key these parameter are.

2. Also, would you continue to have a positive outlook for this policy when the ICR is this low.

3.Can we, as individuals be confident that our claims would be successful on time?

Hi,

Thanks for the detailed comment. While it is apt to point out the ratios as mentioned by you, I am not sure if we understand the story behind.

As for the ICR, it is ideal to have a ratio which is neither too high (low margins for the insurer) nor too low (very high margins and could indicate less claim settlement, but not necessarily). A low ICR can also mean that the company is taking higher premiums for the same coverage in which case it is ideal to renegotiate the premium. As for Royal Sundaram, I don’t see a problem. Probably, it has a larger healthy population not making claims as its customers.

Claims pending ratio could be a result of several factors. I am not aware.

Now I also looked at the claim settlement ratio in the live mint link you have shared, which stands at a healthy 91%. I would consider that as a good ratio.

Hi Vipin

Thank you for this analysis. One of the most helpful I have come across. Mediclaim is like a maze with no finish. I wanted to buy a policy for myself (I am 39 years old) and my daughter. I had narrowed down on Max Bupa health companion. But after looking at your post, I am considering the Royal Sundaram lifeline supreme also. I had a few questions

1) Is it better to go with a govt. organisation or a pvt insurer – from the point of view of faster claim settlemet

2) between Max Bupa health companion/ Max Heartbeat and Royal Sundaram lifeline supreme, which one would you recommend?

Thanks

I guess the most important things you need to look at while selecting your health insurance is whether the insurance has tie ups with the hospitals that you are most likely to visit.

Personally, I don’t prefer any sub limits for room types or diseases or treatments. If that works for you, you may choose a PSU insurer or one such as Star too.

Royal Sundaram seems to have more yes marks for various parameters.

Hope this helps.

Dear Vipin,

Can you help me to find out a best critical care policy for my self aged 42 and my wife aged 39 years .We would like to get a policy for 25 Lakhs with life long renewal.

Regards,

Anil Varghese

Why are you looking for a critical care policy? Any family history of diseases that you want covered?

Vipin,

I don’t have any family history .I am already having United India health Insurance family policy for 3 Lakhs with Top up of 5 Lakhs started in the year 2013. In addition to that I would like to take a critical care and Personal Accident cover policy separately.

Please advise

Hi Vipin, I am looking a 5 lakh health policy for myself and my family,age 42,32,7,2 yrs. I am staying in zone I city.I zeroed on to maxbupa health companion and royal sundaram lifeline supreme. I want to know what is your recommendation and reason for your recommendation. Is there any other low cost policy from public/govt sector like united India, new India insurance ,etc which serves the purpose rather than paying hefty premium to pvt companies. Whether 5 lakh cover is enough considering cost of medical treatment after 15-20 yrs. Whether it is advisable to take separate individual policy for me rather than to club myself with my family.

Between the two that you have shortlisted, Royal Sundaram appears to be a better choice. Read the article to see the difference. There is also a table listing the salient features.

PSU companies do offer but they have several restrictions and lack other features such as restore / recharge. If that works for you, go with them. You should take care of the fact that the insurance company should have hospital coverage in your city.

5 lac cover may not be enough in 15 – 20 years, it is a good number to start with. You can always buy a super top up cover for 10 lacs plus to augment this base cover at a cheaper cost.

Given your current age bracket, you can have a floating cover. Just see what premium difference do you get, if you opt for separate policies.

Hope this helps.

I think i reached right place…..Vipin my self age 30 living in bilaspur chattish -garh loking for a health policy for my family of 3 me ,my wife age 30and my daughter age 3 .Currently i have only employer pprovided health insurance of SI 2 Lac.

Thankfull for your reply.

Hi Avinash,

Hopefully you have got some ideas from this article itself. have you evaluated other policies? What are you expecting from your health cover?

Thanks

I am 50 year old and my wife 42 years , I have health insurance policy of Oriental insurance of 1.5 lakh each . I would like convert into family floater of 5 lakhs. I also would like to add my two sons age 18 and 16 years. shall I use portability and go to private insurance? Please guide

Dear Narayan

Given the age difference, it might be a good idea to take separate policies – one for you for Rs. 5 lacs and one floater for your wife and 2 sons for Rs 10 lacs cover. Please check out possibilities and premium with insurance companies.

You should consider what hospital coverage is available specially in the areas where you are most likely to use them.

Yes, portability should definitely be considered. The Rs. 1.5 lacs of coverage would enjoy coverage for PEDs (pre existing diseases) and no waiting periods. However, the additional cover you take would have to undergo no PED and waiting periods, as applicable.

Consider the overall offer from private and public companies – a few of them – and then take a call.

Dear Vipin,Thank you for your reply , I have a query, how about start heath insurance family optima plan. Is it worth for my case? or would u like to suggest other.

Hi,

I find that the Star policy has several limitations and cappings. You might want to look at their policy wordings on the following link:

http://www.starhealth.in/sites/default/files/brochure/Family-Health-Optima-Insurance-Plan.pdf

You could consider other insurance companies as well.

Hi I am looking for the Family Health Insurance Policy for my parents aged 57 and 50 years for 10 Lakhs. They live in town which comes under Zone-II.

I have finalized Max Bupa Campanion and Royal Sundaram Life Line Supreme. But confused on finalizing the one.

Could you please confirm the below Points.

Which one has Zonal Wise Co-pay?

Which one has Co-pay after 60 or 65 years?

I got the update from Customer care that Max Bupa increase the Premium every year

I am looking for the life time renewal, which one is best?

Which one has good Claim Settlement ratio?

Royal Sundaram has TAP, Is it disadvantage?

Dear Narsi

First thing, consider taking separate individual policies for your parents.

Next, you should find out from both who is willing to give them insurance (considering any pre existing diseases, if any)

Third, look for hospital coverage in the local region. It is ideal to have a cash less tie up with the hospitals they are more likely to visit.

LIfelong Renewal is now guaranteed.

For the points you have mentioned, Royal Sundaram appears to be the choice. It doesn’t have a co-pay.

As far as renewal premium is concerned, most insurers will update the premium, at a later date, when the age slab changes.

Having a TPA would not be a disadvantage, in my opinion.

Hope this helps.

Thanks Vipin.

I heard of a case of Apollo rejecting a claim because the applicant forgot to declare that he had a viral fever a decade back. They claimed he didn’t correctly declare his history, so they denied his claim, and canceled his policy, without even refunding his premium.

If Apollo is going to play such games, better not go with them. I think it would be good to update the post with such practical matters, not just what’s written in the policy documents.

I have been reading your portal and many other portals and its really great of all of you interms of efforts you have put. I have gone through the plans but i’m still stuck and need your help on this.

I have a health insurance for my father & mother for SI of 3 Lakhs from United India. But it is very less. Since the policy is in renewal stage i cannot port it now.

My issues are:

1. UI basic policy has too much sub-limits. I want it to port it to Max Bupa health companion or royal sundaram lifeline. Confused betwwen 2.

As max bupa has negative reviews and 20% co pay for tier 2 cities ( which is applicable in my case for my parents). Hospital network is also limited. Whereas Royal sundaram is new in this. Can’t take others as my father is 69 years and also premium is much high for apollo and Religare ( religare also has a co pay).

2. Will it be useful to have a top up of 5 Lakh with 2 Lakh deductible with United India ( same insurer of base Policy)? Because the Basic Policy SI is of 3 Lakhs has sublimits and if claim is close to 3 Lakhs ( SI) I’ll have to bear expenses out of pocket.

In this case ( claim amount is between 2-3 lakhs) though base policy SI is 3 Lakh whether the Top up will be applicable if i choose 2 Lakh as deductible for the top up? or will it be applicable only once the base SI of 3 Lakhs is exhausted?

3. I’m also planning to take super Top from UI only with 15 Lakhs cover and 5 lakh deductible ( since top up will cover till 5 Lakhs).

Please suggest. As i’m finding this is the cheap and best option. Not sure if I’m missing any vital point.

Best Regards

Nishant

Nishant

If you port the policy to another insurer, you will get a full continuing cover on Rs. 3 lacs with additional benefits, if any. Keep that in mind before you go for a super top up or top up.

For point no. 2, it’s best to confirm with UI what their policies are.

Between topup and super top up, go for super top up, if you have to. If you take additional top ups, they have to wait for the Pre existing diseased and other waiting periods for slow growth diseases.

I would have tried to keep it simple, instead of cheapest. First strengthen the base policy. Port the UI policy to Royal Sundaram (it also offers a 15% discount on premium for Tier 2 cities) for 5 lacs at least. The 2 lacs will have to do the normal waiting for diseases. At this stage, keep the policies for both parents separate and not a floater. The needs can be a lot more than you think.

Then take a super top up, if you still feel so.

Hope this helps.

Waiting periods are not there in group mediclaim policies provided by employers, but room sub limit may be there.In Religare care policy, single private room is eligible, but waiting periods are there. In modified version of CARE called – CARE V2 – waiting periods are reduced / removed with additional premium. In Religare there is no TPA. Direct settlement.

This article is the best starting point I have come across, to pick a medical insurance policy.

I would add a few conditions:

– I would want there to be no waiting period (like 2 years) for specific diseases. If I pay the insurance company this year, I expect coverage from all diseases this year.

– I won’t get a medical test done (I’m in my 30s) to get insurance, since it’s an unnecessary hassle for me.

– If possible, no TPA.

I would relax a few conditions:

– If the company says I’m eligible for the cheapest private room, that’s fine. I don’t need a suite, and won’t use one even if was eligible.

I would keep your other conditions:

– No deductible

– No co-pay

– No disease-based sub-limit

– No geography-based sub-limit

Does anyone know a policy that meets these conditions?

As of now such a policy doesn’t exist, at least in my knowledge.

For waiting periods, any accident related issues are covered immediately from Day 1.

As for tests, typically there are not tests done if a policy is taken before 45 years of age.

TPA is only a business process outsourcing. Not sure if it makes a huge difference.

Thanks.

Dear Vipin

I have RELIGARE CARE policy for Rs 25 lakhs taken two years before with Super NCB. It was one of the best policy during those period.For Rs 10 lakhs and above, room rent limit is Single Private room upgradable to next level. Organ donor cover is Rs 2 lakhs. However there always exists some uncertainty in eligible room availability during exigencies.

Max Bupa’s health companion & Royal Sundaram Lifeline Supreme has no Limit or capping on any account in room rent/ Donor cover/ alternate treatments, etc. Currently CARE premium is higher(Recently Religare increased premium).I has not made a claim till date. Is it advisable to port to Royal sundaram or Max Bupa from CARE? or to continue with CARE? Please advise.

Dear Satheesh

The concern about the room type always remain. If you are not comfortable with it, you might like to port. I would go with Royal Sundaram.

Thanks for the comment. Hope this helps.

I’ve Health insurance coverage from my employer with “United India Insurance Co. Ltd.” and we’ve Portability option even if we leave the company. That meas we can continue with the this insurer even after resigning and below are the features will be covered.

1) With stadard benifits

2) Pre-existing conditions will not be applicable as I’ve completed the pre-existing period (3 or 4years) with my current employer

Is it suggestible to continue with the same or shall I take one more out of employer? I was trying to contact on “United India Insurance Co. Ltd.” customer care number but could not connet (either number does not work or waiting or not picked up).

Please suggest.

Dear Santosh

What you should take into account is the amount of cover that you have already and what you will need? If you have a 4 lac cover, would that be enough or you would need a 10 lac cover for your family.

Then, understand the limitations or exclusions, if any.

For example, IF you have a 3 lac cover, typically a 1% of that is allowed for room rent / day and 2% for ICU room rent/day.

Also, you might be getting a maternity benefit under a group policy but that is excluded from most private covers. Some would allow but for a higher premium.

If you are falling short on above expectations, then you must take a separate cover for yourself. Hope this helps.

Thanks Vipin for the feedback. I hope, I can increase the coverage whenever I’ll leave the company as the premium also will be changed as the policy will become individual from group plan. My supporting points/concerns are below

Pros:

* No Pre-existing period which is 3 or 4 years depending on insurance provider.

* Pre-medical tests with max of Rs. 375

* So far claim ratio is very good (not sure whether it is bacause of part of large organization and will be treated same when becomes individual but so far, 9 years, experience is good)

Cons:

* I was trying to contact customer care but never call was picked up or working the number provided on the portal. As it is a govt insurance company, how they will answer queries in future? Now we’re contacing thru 3rd party but not dircetly to United Insurance staff.

Santosh

Remember, whenever you increase the cover, the fresh waiting periods will be applicable on the increased cover. So suppose, you have a 3 lac policy today and when you port out you want a 5 lac policy. On this extra 2 lac, you will have to suffer the 3 or 4 year waiting periods and other exclusions as applicable. Just FYI.

Premedical tests are applicable to individual policies also? I doubt.

As for claims, you usually contact the TPA. IN most cases it is cashless as well. You contact the issuance company only for buying the policy and receiving the documentation.

Hope this helps.

Thaks Vipin. Waiting period for extra amount is fine for me as I never used the whole amount so far. Regarding maternal benifit, I do not need any more 🙂

For claims, contacting TPA is fine but if I want to know some info like on the policy terms after leaving the company, we need to contact insurance company directly, right?

Most terms are mentioned in the document. If you want to know anything more about the policy, you can contact the insurance company. For claims, you need to contact the TPA.

Hi Vipin

I am about to buy a policy from BUPA or SOMPO. can you comment over claim settlement/ support from company by Mex BUPA/ SOMPO after sale of policy.

reviews on mouth shut .com are very negative????

In SOMPO they consider first heart attack as a critical disease , what is this?

Regards

Asheesh

Hi Asheesh,

As per my assessment, Max Bupa may not make sense.

I believe Sompo doesn’t have as comprehensive a coverage. The First heart attack covered under SOMPO will be a part of the Critical Illness rider with the main policy. Don’t opt for riders. Buy only mediclaim.

You have to evaluate a policy on what fits your needs. You might want to pick one of the 4 compared in the article.

Thanks

Vipin

if ones policy is terminated can you port that policy ?

No. Only an current existing policy can be ported.

Vipin,

What’s your view on Royal Sundaram – Lifeline Supreme? Am looking for health insurance for my parents.

Well, if it helps, I just took this policy for my parents too. 🙂

What about ICICI Lombard’s iHealth Complete Health Insurance?

Can you find some flaws & pros of the Plan?

I am a 28 yrs old want a Individual Policy of 5-10L SA. Can you suggest me a policy thats suits me.

I could not find out the No claim bonus working or features like Restore, Recharge, etc for ICICI policy? Have you got a quote from them for the premium?

You should also consider Religare and Apollo policies. Thanks.

Hi,

Can you please provide your comments/ suggestion of Universal Sompo Complete Health Insurance.

Dear Biren,

Universal Sompo CHI is quite similar to Apollo Restore. The only thing to note is that the Restore Benefit will click on only after you have exhausted the Basic Sum Insured. See one of the comments below to know how it can impact your claims.

There is also a maternity benefit but I think paying a higher premium to take this benefit almost as long as you continue the policy, that too with a initial waiting period of 3 years to file your first claim, may not be a beneficial option.

I am not sure of the premium being charged on this policy.

Thanks.

Thanks, Vipin, for this article. Medical insurance is such a mess, and you’re making it slightly comprehensible.

Regarding increase of premium based on claims, as I understand it, the government permits the insurance company to do that for a class of users (men in their 30s, for example) if that class makes lots of claims, not based on an individual’s claim history. I don’t see any contradiction between what the terms and conditions are saying and what the government allows them to do.

Thanks Kartick for the comment.

You are right it shouldn’t bother much. It was just a matter of being aware hence mentioned in the post.

I have realize that in terms of education people are more aware about mutual funds as compare to mediclaim.

In mutual funds, i have found DIY kind of investor but in case of mediclaim i am yet to find DIY kind of insured person.

You couldn’t have said it better. Mediclaim is a mess. Thankfully, several companies have made a lot of features easier to understand. As I also mentioned, when you call up these companies, the agents at the other end are very patient in helping you understand the policy in great detail. Of course, one has to know the right questions to ask.

Vipin,

I was just waiting when you would write something on health insurance (a topic which is very close to my heart).

Your analysis is really comprehensive.

Taking your 3 policy as a base, here are my additional comments:

1. The most important factor which i consider is “No limit on room rent”. So going by this, Religare becomes my 3rd preference bcz it still has a room rent limit of “Single Private room”.

2. Other than the room rent part, most of the opther benefits of these 3 policy are same with slight difference here and there.

3. Also when you are comparing the premium of “Apollo Optima Restore”, it better to compare with “NCB super”of Religare instead of “care” of religare. Bcz “care” from religare is somwehat equivalent to “Easy health – standard” of apollo and “NCB super” from religare is somewhat similar to “Optima restore” of apollo.

4. Out of these 3 my 1st preference would be apollo then max and then religare.

5. If its a clean body (a body with no PED), then i would go with apollo but if someone has any kind of PED, then i would not go with Apollo bcz most of the time apollo will put that PED as permanent exclusion which is not good for the client, rather i will go with Max.

6. If you compare the premium of “Easy health – standard” of apollo then it is in line with other two policies which you have mentioned.

Thanks Dinesh. I hope as a first piece, I have been able to cover it adequately.

You have made some relevant observations.

Now, I understand “No limit on room rent” is the ideal situation. But as long as a Single Private Room is available it is as good if not better. There is practically no limit on the room rent. I would be happy to have this as an option too.

Your are right about NCB. The Super part of Religare is more comparable with Apollo Optima Restore. I believe i have mentioned this in the pointers later in the post.

The fact that Apollo would take any pre – existing diseases as a permanent exclusion is news to me. As per their policy wording, PEDs are covered after 3 years. I am sure you must have experienced this, hence your comment.

Easy Health of Apollo doesn’t have the “Restore” feature which is a part of the 3 plans compared here.

Thanks again for the comment. You have made the post better. 🙂

Its not that every PED will be put under “permanent exclusion” by apollo.

Ofcourse PED will have a waiting period of 3/4 years depending from company to company, but if the underwriter of apollo feels that PED is more serious then that can be put as a “Permanent exclusion”.

The important part is as of now its only with apollo i have experienced this “permanent exclusion” otherwise in other companies either they reject the case or else accept it with a waiting period of 3 to 4 years with some extra loading.

Thanks again for the comment Dinesh. I confirmed with Apollo about the Restore feature too. You are correct about how it works. I am also considering another interesting plan with Royal Sundaram – Lifeline Supreme. Any view on that?

No vipin,

Royal Sundaram is not in my research list.

I have restricted myself to Apollo, Maxbupa, Bajaj, Religare and L&T.

Reason being i am yet to come across a feature which these companies are not offering.

Also i do not want to complicate the things for me as well for my client.

For the time being, i am more than happy with these companies.

Dear Vipin,

Wonderful article, I was doing some comparison before I buy a health insurance plan and happened to see your blog. I too had narrowed down on Apollo Munich.

Just wanted to add about the ‘Single Private Room’ clause… Chances are there that none of the Single private rooms are vacant and this would mean we either look for an available room a notch above or below. If we decide to opt a notch above then the room rent will not be covered by the insurance, plus the medical expenses, doctor fees, nurse fees increase as we scale up the room’ grade. I am not very sure if this delta also be covered by the insurance party.

Thanks for the comment Shyam. Pardon my ignorance, but I am not sure if there is something above a “single private room”. Is there?

Wow Vipin, that was super quick. Yes we do have a lot of categories among room especially in big hospitals. for example I have pulled out the different options we have at Apollo Chennai.. It starts from General ward and ends up in Suite room 🙂

Source : http://chennai.apollohospitals.com/hospitals/greams-road/facilities

General Ward

Special General Ward

Double Sharing Room

Semi Private Room

Single Room

Deluxe Room

Executive Room

Suite Room

Apollo Suite

Got it! Thanks for the information.

I was mulling up the various options so that I have the right mix of group insurance provided by my employer, health insurance taken by me and Super Top up. I thought of putting it over here so that I get opinions from you and other fellow readers.

I am looking for an Individual policy and fall under age bracket 36-44

QQ1) In Apollo Munich Optima Restore, are there any differentiation between the facilities offered with respect to SI? meaning will there be additional benefits to someone opting a policy with SI 15 lacs than those who opted a policy with SI 3 lacs?

QQ2) Which of the below combination makes sense and why?

Company provided group policy – SI 3 lacs

Apollo Super Top with SI 7 lacs and deductible 3 Lacs (Premium 3195)

or

Company provided group policy – SI 3 lacs

Apollo Optima Restore – SI 3 lacs (Premium 6662)

Apollo Super Top with SI 5 lacs and deductible 6 Lacs (premium 1940)