The doorbell rang, twice. I open the door and I see Sachin, my neighbour, standing there. He stared at me and then quickly walked into my house.

“Vipin, I read your posts on equity mutual funds and debt mutual funds. I also read about asset allocation and diversification.” Sachin said, as he took a seat.

“But you know, I still can’t figure out how to build my portfolio of debt and equity funds. It is all getting too confusing – choosing equity funds, then debt funds.

Can you tell me just ONE fund that can take care of both debt and equity investment?” I now understood the purpose of the sudden visit.

“Ah, my friend, I understand your pain. I guess even the mutual fund houses understand it too. So, they made something to solve exactly your problem.” I replied.

“You mean to say something like that actually exists. That’s great! What is it?”

“Sure Sachin. I am not sure if you have heard of Balanced Funds. These funds are mandated to invest in both equity/stocks and debt such as corporate debt and government securities.

The name ‘balanced‘ might suggest that they invest 50:50 in equity and debt. But that is not the case. I think they are better off being called Equity-oriented hybrid funds. Equity-oriented because a major portion of the fund is invested in equities. The equity portion is typically 65% and above.

The big reason for this 65% allocation is to become eligible for the taxation benefit similar to equity mutual funds. If the fund has less than 65% of the portfolio in equities, it would be treated as a debt fund and would attract taxation accordingly.

Now Sachin, I know you are a moderate risk taker. From that perspective too, balanced mutual funds or equity hybrids offer a super opportunity for investors like you to take exposure to debt and equity in just one fund. The presence of debt along with equity offers a compelling moderate risk investment option.”

“That’s what I want, Vipin. Great! Tell me more.”

“Here are some more benefits.”

Balanced Mutual Funds – Best of both the worlds

- One fund for both equity and debt investments – That is the simple beauty of it. You don’t have to make separate investments in debt funds and equity funds. One fund takes care of both. IF you do not want to get into the hassle of two different types of funds, balanced mutual funds are for you. For your goals such as retirement or your children’s education, you can invest in a balanced fund.

- Automatic asset allocation and profit booking – You don’t have to worry about changing allocations between debt and equity or to buy and sell stocks or government securities and bonds. It is all done within the fund. It is a beautiful way to balance the upside as well as the downside. In a scenario, where equity markets rise a lot, the fund manager will simply book profits and get the allocation back to 65% by investing the money in debt. When the markets go very low, the fund manager will pull the money from debt and invest in equities, so that the allocation remains at 65% or above.

- No Long term Capital gains Tax – Even though a portion of the fund is invested in debt instruments, the overall taxation is still like equity funds. That means if you sell after 1 year, there is no long term capital gains tax. In all debt funds that is not the case. If you sell within 3 years, you have to pay short term capital gains tax at the rate of tax applicable as per your income tax bracket. If you sell your debt fund after 3 years, 10% capital gains tax (before indexation) is payable.

“Vipin, I think it is a complete no-brainer now. Before I lose my balance figuring out equity and debt, let me invest in a balanced mutual fund. Can you tell me which one is right for me?”

“That’s where the difficulty starts. There are several balanced funds out there and in many flavours. Almost every Mutual Fund company has at least one scheme. Choosing one over the other is an exercise in itself.

We will have to do a little filter process here. Are you ready for it?”

“Yes, of course.” Sachin was excited.

“Would you like some tea, Sachin?”

“Can I ever say NO?” was the prompt reply, with a smile.

Selecting the right Balanced mutual funds

So, I went about the selection process based on the previous criteria. This is what we did.

We downloaded the balanced mutual funds data from Valueresearchonline. The data is as on September 30, 2015.

There were 48 balanced fund schemes. We had to apply some filters to prune it down to the most relevant ones.

- The first filter was for the age. All funds with less than 3 years of existence were removed. They need more time to build a track record. This eliminated 14 schemes.

- The second filter was the Expense ratio. All schemes with over 2.5% expense ratio were eliminated. 22 schemes got removed with this filter.

- Schemes with Net Assets of less than Rs. 100 crores were also eliminated. This removed 2 schemes.

- Finally, Schemes with a Turnover Ratio higher than 100% were eliminated. There was just 1 scheme that got eliminated here.

- Since the portfolios also have a debt component, we looked at the Credit Quality. Thankfully, the credit quality of the debt portfolio is High with most investments in AAA rated Corporate Debt or Government securities.

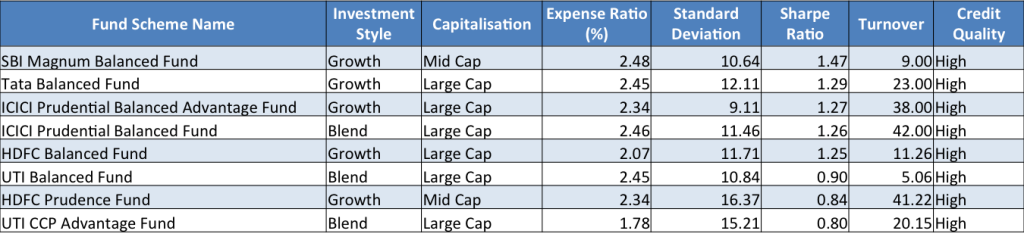

So, finally we were down to a list of 8 balanced mutual fund schemes.

Here is the final list.

As you can see, the two mid-cap oriented funds from HDFC and SBI tend to take on higher risk and also deliver higher returns.

Within a mutual fund house, you can also see more than 1 scheme. For example HDFC. HDFC Balanced Fund invests its equity portion in large-cap stocks, while its Prudence Fund goes after mid-cap stocks.

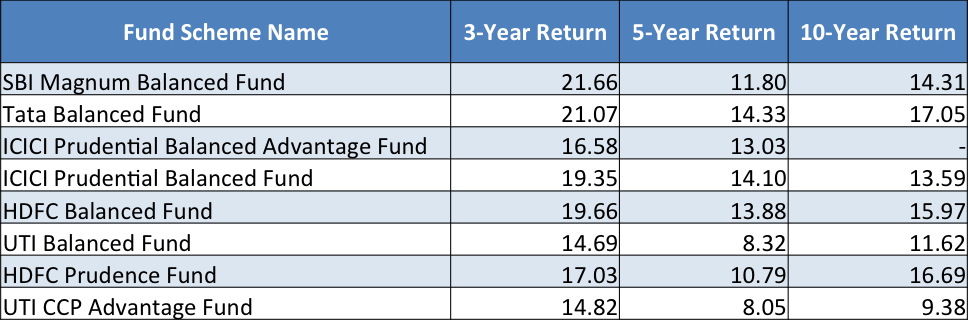

And here is how they stack on returns.

To reiterate – returns is not a part of the selection criteria.

And now the fun begins.

“Which fund will you choose to invest in?” I asked Sachin.

“That’s what I have come to ask you, Vipin.”

“I know. But here is an opportunity for you to learn. You have seen the process that we have followed till now. You have to now make the final choice. What will you put your money into?”

“Hmm. OK. Give me some time to think and get back.” Sachin stood up to go out. “I feel I know my answer but I just want to ponder over it for some time. I will surely let you know.”

“Sure. I will look forward.”

“Thank you for the tea”, he said, closing the door.

While Sachin gets back, let’s (you and me) convert this search into an interesting learning exercise. Use the comments section and suggest which fund would you choose to invest in along with the reasons? I am waiting for your response.

Disclaimer: The list of mutual fund schemes provided above is for information purposes only. Please check with your investment advisor to know which fund scheme is correct for your time horizon and risk appetite. Mutual fund investments are subject to market risk. Past performance may not be sustained in the future. Please read the scheme information documents carefully before investing.

My dear bipin…I have serfed so many sites regarding m.f. but the way you explained it is fantastic.very easy to understand..thnx

Thank you Rajan. You have encouraged me with your generous comment. Keep reading.

Hi Vipin,

as usual great article.. just direct to the point even to newcomers.

one question – though it may be kinda silly, why are always 3 years average returns around 18-25 percentage, but 1 year returns or 10 year returns 5-15% or sometimes negative.

I get that it is average of the returns every year, but does it mean if I had invested in ANY of the funds and taken my money out in 3 years I would have got around 18-20%?

thanks

Hi Sreenivasan,

The returns that you see in the charts/tables are point-to-point. Means that they are measured from, for example in case of 3 years, the value 3 years ago and the value today. So if the value 3 years ago was Rs. 10 and today it is Rs. 20, then the return would be shown as 24%. It does not take into account any ups and downs in between. If you had invested Rs. 10,000 in one single day 3 years ago, this is what you would have got.

However, usually, that is not how you invest in real life. You invest at various points, monthly, yearly, quarterly or as and when you can. A simple example is a Systematic Investment Plan or SIP.

So, you purchase at different values at those points and your cost of purchase gets averaged out while your entire portfolio value today would be determined by the per unit market value today. And this result could be very different than the point to point return that has been shown in the table.

Just as an FYI, these returns are only indicative. Hope this helps. Thanks.

I am clear its will be HDFC Balanced fund for me considering balance of all parameters of risk, volatility, cost and turnover.

regards

Great choice Jinesh. Thanks for the comment.

Day by day you are increasing my interest towards ‘money matter’ and every new topic inspires me to search the details and gain little bit knowledge. When you posted debt fund blog, I was about to ask you to write on balance funds.

One suggestion though! it is good and politically correct to give a list of funds and allow user to decide based on their own intuition and knowledge, but I feel there might be users (like me) who trust and relay on your opinion, so it would be helpful if you end you blog stating, these are my final two choices based on this criteria, what are your? because choosing 1 or 2 from 8 is still a big task for the user considering his limited knowledge/experience!

Can you start making Youtube videos? It would be interesting to see your knowledge in interactive mode 🙂

Can you at least give us the list of upcoming subkects that you are going to write?

Am I asking too much…pls excuse !

Thank you for this article!!!

Thanks so much Umesh.

While I agree that I should not leave a reader like you in limbo, I have a purpose in doing so. The purpose is that those who are really interested would in any case write back to me and I would be happy to let them know the funds 🙂

Youtube videos – you almost read my mind. I am planning one very soon on a topic that you only had suggested. Bravo!

I don’t really have a list list. I keep looking at reader queries or divine inspiration to shortlist a topic and write on it. 😉

Always keep asking, my friend.

Thanks

I really like the way you start the topic making the reader more comfortable (better say more friendlier and related to the topic) and explain things.. nice write up Vipin!

Thank you Rajesh. Glad you liked it. Hope it is useful too.