A question that I was recently asked with regards to investing in equity mutual funds was whether a fund should be fully invested in equity at all times or should it be holding cash if need be?

There were two arguments against a stay in cash strategy.

One, holding cash can lead to underperformance as the markets may rally faster than the funds can search for opportunities and deploy the cash.

Two, how can a fund hold cash and charge a Fund Management fees of 1% to 2% or more? The investor pays fund management fee to make investment in equities, not for holding cash.

Let’s see if these arguments hold any water.

Why is a fund holding cash in its portfolio?

Point 1, a fund needs to hold some cash to meet short term liquidity needs such as redemptions, etc. This is typically a lower portion of the portfolio, about 2% to 3%.

Point 2, some funds hold cash as a part of their investment strategy or their inherent nature.

Such funds fall into 3 categories:

- Dynamic Funds: They intend to switch to debt or equity based on their assessment of overall market valuations. They move the portfolio across asset classes. When equity valuations turn expensive, they add on a lot more debt/cash and vice versa. E.g. ICICI Pru Dynamic Plan

- Hybrid Funds: Here we refer primarily to hybrid equity funds here. They are also known as balanced funds. These funds have a minimum of 65% invested in equity and the remaining in debt or cash. They rebalance the portfolio between debt and equity to maintain the hybrid nature. E.g. HDFC Prudence Fund

- Value focus funds: These funds do not buy unless the a business is available at the right price, at least as per their evaluation criteria. E.g. Quantum Long Term Equity Fund

What is the result of the ‘holding cash’ strategy for each of these funds? Does the performance suffer?

Let’s use some data.

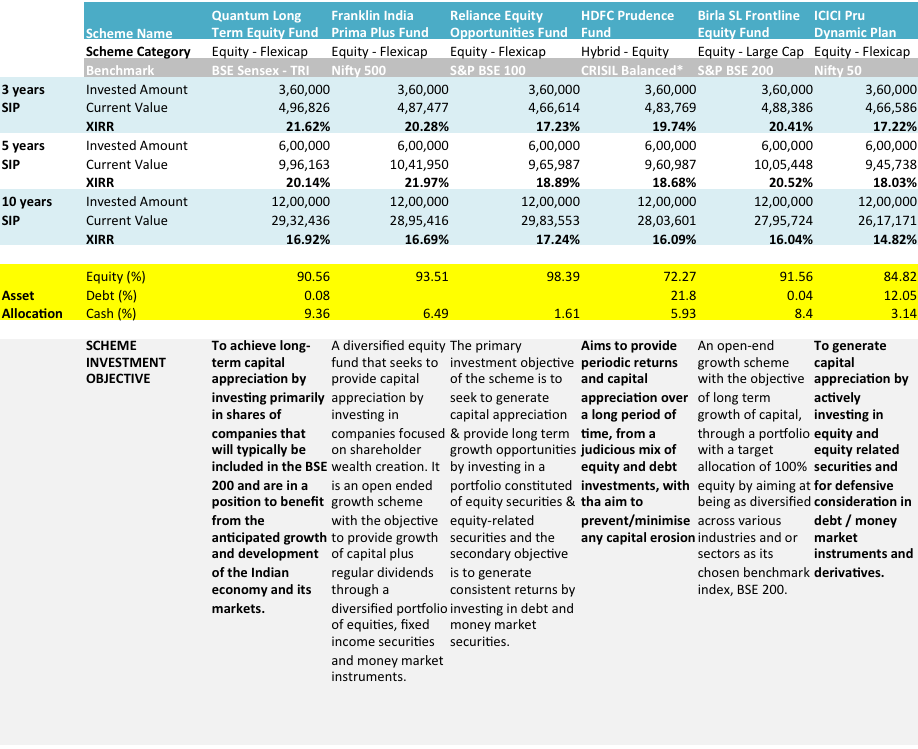

Take a look at the following table.

DOES HOLDING CASH AFFECT PERFORMANCE?

Data Source: smart.unovest.co; HDFC Prudence’s benchmark is CRISIL Balanced – Aggressive Index.

As you can see, there are 6 funds – 3 Flexi caps (Reliance Equity Opportunities, Franklin India Prima Plus, Birla Sunlife Frontline Equity) and 1 each of the categories identified above, that is, hybrid-equity, dynamic plan and value focus.

These funds are some of the most popular funds given that they command large Assets Under Management or follow the ‘holding cash’ strategy to the hilt.

Only regular plans have been considered to study data over longer periods. Direct plans were started only from Jan 1, 2013.

For reference, the stated investment objective and the current asset allocation of the funds is also included.

The SIP performance of the funds over past 3, 5 and 10 year periods is mentioned. The SIP amount is Rs.10,000 per month. The performance is measured backwards for the stated time period and starting August 2016.

To put it in context, in December 2014, Quantum Long Term Equity was holding cash to the extent of over 30% of its portfolio. Even as recent as December 2015, the cash holding in the fund was over 10%.

Did the performance suffer because of holding cash?

Based on the selected funds that we studied, it appears that, if done right, holding cash is not working against funds holding cash. Except for ICICI Pru Dynamic Plan, which faltered on its performance.

Quantum’s fund, despite having significant cash holdings, has managed to deliver a performance at par or sometimes better than its peers.

Compared to the ICICI Dynamic Plan, HDFC Prudence has done a much better job. As a hybrid fund, it has deftly used equity and debt to deliver a superior performance.

Another noteworthy effect of this strategy is that these funds are able to reduce volatility in their portfolio and provide better risk-adjusted returns.

Exercise for you: Which data points would you look at to measure risk-adjusted returns?

What about the investment management fees on the cash portion?

The response by a fund manager to this question goes like this – the decision to sit on cash and wait for the right investment opportunity is also a fund management decision. Investments are made at the right price, as and when they are available.

What should you do?

Should you be worried about a fund holding cash or not? Frankly, it’s a choice you have to make.

Any fund that does not deliver, with cash holding or without, would be a matter of concern. If you continue to believe in the fund house, the scheme, its investment objective and its process, stick on. Else, you can always move your money to another one.

Remember though, funds that hold cash, may underperform in the short term. That’s a given.

Unsolicited advice: Do not evaluate a mutual fund on the basis of just 1 or 2 year performance.

As for the fund house, it would be great on their part, to be upfront and accept that they cannot find enough opportunities and hence return the cash to the investors.

Probably, that is too much to ask for. Well, if they don’t, you can always press the redeem button.

What would I do?

As for myself, once I have identified my funds, I would let the fund manager(s) take specific investment decisions. Even it if means sitting on cash, so be it. At the end of the day, the results will speak.

My vote is with holding cash as a part of the investment strategy. I have no problems with it.

What’s your vote? Do let me know in the comments.

@kartic in practicality buying one stock till a new one is again equivalent to timing. You are saying that 2 coincidence should occur at the same time. One, the stock you wish to go long should reach a level where you want to buy and the stock purchased should be at the right price where you can sell (obviously positive)? On the same day and at the same hour? Doest look that easy as prices are too volatile. I would like my fund manager to earn 7% till he sees a kill in the market.

And, about holding cash I think if you are a value fund manager, cash is what leverage you in comparison to a momentum-pick fund manager. Your thoughts?

I agree with your points, which are insighful. Thanks.

This is too small a sample size. Ideally, one should plot all funds in India to see if there’s a correlation between holding cash and fund performance.

Yes, you want to make me work a lot harder 🙂

Excellent write-up Vipin, as always. Cash is an asset too in the MF portfolio. Besides maintaining the portfolio liquidity, it creates an opportunity as well as hedge portfolio in adverse times. although this was a known fact but you proved it using the data. Great!!!

Warren Buffett says that Berkshire Hathaway always has at least $20 billion–and usually a lot more–in cash equivalents.In fact, it rose to 55 Bn$ in 2004. Look at the returns they made for investors.

Thanks for reading and the comment Madhupam.

Interesting points, Madhupam. Regarding your point that cash creates an opportunity, I suppose investing that money in some other stock doesn’t preclude the fund manager from later selling it and taking a better opportunity that comes along later.

Holding on to cash, say investing it in a liquid fund that fives 7% return, makes sense only if the fund manager can’t identify any opportunities that are expected to give a higher return. Would you agree with that, Madhupam and Vipin?